Market Overview:

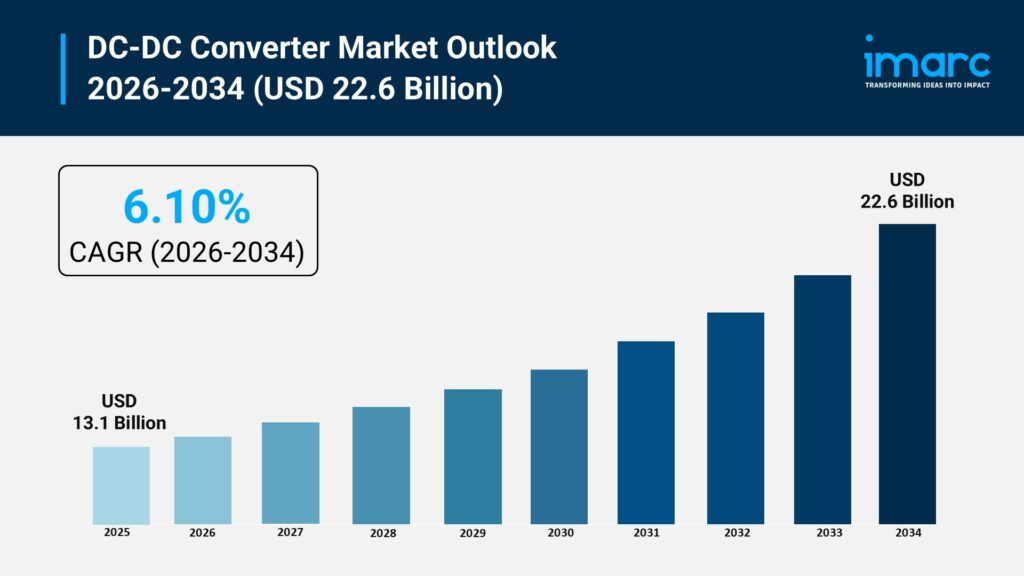

The DC-DC converter market is experiencing rapid growth, driven by rapid electrification and EV architecture shifts, expansion of 5g and digital infrastructure, and industrial automation and renewable energy integration. According to IMARC Group’s latest research publication, “DC-DC Converter Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034”, The global DC-DC converter market size reached USD 13.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 22.6 Billion by 2034, exhibiting a growth rate (CAGR) of 6.10% during 2026–2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/dc-dc-converter-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends And Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the DC-DC Converter Market

- Rapid Electrification and EV Architecture Shifts

The aggressive global transition toward electric mobility serves as a primary engine for the electric vehicle high voltage DC-DC converter market. As automotive manufacturers migrate from traditional internal combustion engines to battery electric and hybrid platforms, the requirement for sophisticated voltage regulation has intensified. Modern battery electric vehicles frequently utilize upward of 50 to 100 individual DC-DC converter instances to manage power distribution between high-voltage traction batteries and low-voltage auxiliary systems like infotainment and safety sensors. In early 2026, leading Tier-1 suppliers announced integrated power distribution units that combine DC-DC conversion with energy arbitrage capabilities, shifting the market toward higher-value system integration. This demand is further solidified by the commercial vehicle sector, where electric buses and Class 6-8 trucks require high-power converters exceeding 10 kW. Currently, the pure electric vehicle segment accounts for over 58% of the propulsion-related market share, necessitating robust, high-efficiency conversion solutions to maintain vehicle range and safety.

- Expansion of 5G and Digital Infrastructure

The global rollout of 5G base stations and the surge in hyperscale data center construction are creating massive demand for high-performance DC-DC converters. These digital environments require precise voltage regulation to support advanced GPUs and AI accelerators, which operate at low voltages but extremely high current densities. In 2026, data centers are increasingly distributing power at 48V to reduce transmission losses, requiring localized DC-DC converters to step this down to the 1V or 5V levels needed by computing hardware. Telecommunications investments are equally impactful; 5G infrastructure necessitates wide-input-range converters capable of operating in harsh outdoor environments. Major industry players like Monolithic Power Systems have responded by launching 48V-input multi-phase buck converters specifically for AI servers, achieving peak efficiencies of 96.8%. This segment is bolstered by the 100–500V input voltage range, which is becoming a dominant market standard for both telecommunications and automotive power stages.

- Industrial Automation and Renewable Energy Integration

The push for smart manufacturing and decentralized energy systems is driving the adoption of industrial-grade DC-DC converters. In industrial automation, robotics and motor control applications rely on these converters for stable energy management, with companies like Magnachip expanding their portfolios in 2026 to include high-performance MOSFETs and IGBTs for these specific fields. Simultaneously, the integration of renewable energy sources, such as solar photovoltaics and wind power, requires DC-DC converters to interface variable DC outputs with battery energy storage systems and microgrids. This shift is characterized by a move toward “Power Electronics 2.0,” which incorporates smart grid integration and distributed control architectures. Current market data indicates that the Asia Pacific region, led by China’s massive 5G and charging pile infrastructure, captures over 55% of the global market share. Government initiatives focusing on clean energy and energy-efficient industrial standards are accelerating the replacement of legacy silicon components with advanced power conversion technologies.

Key Trends in the DC-DC Converter Market

- Adoption of Wide Bandgap Semiconductors

A defining trend in the current DC-DC converter market is the transition from traditional silicon to Wide Bandgap (WBG) materials, specifically Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials allow converters to operate at significantly higher switching frequencies—often exceeding 500 kHz—while maintaining thermal stability. In 2026, GaN-based converters are achieving power densities over 50 kW/L, which is roughly 3 to 5 times higher than silicon-based counterparts. For example, Infineon Technologies recently unveiled a GaN DC-DC converter family optimized for 400V-to-48V conversion in electric vehicles, reaching a peak efficiency of 98.1%. This trend is particularly critical for mobile and aerospace applications where weight and size reduction are paramount. The use of SiC MOSFETs in traction inverters is also becoming standard, as they can reduce switching losses by nearly 50%, directly extending the operational range of high-performance electric machinery and vehicles.

- Integration of Bidirectional Power Flow

The emergence of bidirectional DC-DC converters is reshaping how energy is managed in vehicle-to-home (V2H) and vehicle-to-grid (V2G) applications. Unlike traditional one-way converters, these advanced systems allow power to flow both from the source to the load and back again, enabling electric vehicles to act as mobile energy storage units for residential or grid stability. This trend is supported by new regulatory mandates, such as the EU’s Ecodesign Regulation, which requires auxiliary power systems to meet minimum efficiency thresholds above 96%. Companies are now qualifying high-density synchronous buck-boost converters that handle wide input ranges (e.g., 2.8V to 80V) to facilitate this two-way energy exchange. Real-world applications include smart homes where an EV’s battery provides backup power during peak demand, managed by a bidirectional DC-DC interface that ensures seamless transition and high energy recovery during regenerative braking or grid discharge.

- Digital Power Management and Telemetry

DC-DC converters are evolving from simple hardware components into “data nodes” through the integration of digital control and telemetry. Modern converters now feature PMBus interfaces and integrated sensors that provide real-time data on efficiency, thermal health, and load conditions. This digital transformation allows for predictive maintenance in industrial settings and precise power tuning in high-density computing environments. For instance, Renesas Electronics recently secured a $320 million design win for multi-phase automotive buck converters used in next-generation ADAS domain controllers, which utilize digital feedback loops to ensure stability. This trend also encompasses the use of software-defined power architectures, where converter parameters can be adjusted via firmware to optimize performance for different workloads. This shift toward intelligent power management is essential for the 2026 landscape of AI-driven data centers, where even a 1% gain in conversion efficiency can result in significant operational cost savings.

Leading Companies Operating in the Global DC-DC Converter Industry:

- ABB Ltd

- Bel Fuse Inc.

- Delta Electronics Inc.

- Fujitsu Limited

- General Electric Company

- Infineon Technologies AG

- Meggitt plc

- Murata Manufacturing Co. Ltd.

- RECOM Power GmbH

- STMicroelectronics

- TDK Corporation

DC-DC Converter Market Report Segmentation:

By Mounting Style:

- Surface Mount

- Through Hole

Through hole represents the largest market segment as it provides enhanced mechanical support and reliable electrical connections for durability in various industries.

By Input Voltage:

- 5–36V

- 36–75V

- 75V and Above

5–36V accounts for the majority of the market share due to its versatility in adapting to a wide range of applications across different industries.

By Output Voltage:

- 3.3V

- 5V

- 12V

- 15V and Above

5V holds the biggest market share as it is widely used in consumer electronics and aligns with standard USB voltage specifications, making it essential for many devices.

By Application:

- Smartphone

- Servers PCs

- EV Battery

- Railway

- Others

Smartphone dominates the market segment as DC-DC converters are crucial for providing stable power supplies and enhancing performance in modern smartphones.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific exhibits a clear dominance by accounting for the largest DC-DC converter market share, driven by rapid growth and demand in the region.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302