Business Loan Rejected Due to No Collateral? Here’s How Businesses Can Still Get Funding in 2026

In today’s competitive financial environment, getting a Business Loan approved has become increasingly difficult for startups, MSMEs, and growing enterprises that do not own property or fixed assets. Across India, thousands of profitable companies face rejection simply because they cannot provide collateral security to lenders.

Traditional banks and NBFCs still prefer secured lending models where land, buildings, or commercial properties are pledged against funding. As a result, many businesses with strong revenue, healthy cash flow, and expansion potential fail to access capital at the right time.

However, the funding landscape is changing rapidly in 2026. Modern financing models, collateral partnerships, third-party security structures, unsecured lending, and alternative funding solutions are helping businesses overcome loan rejection challenges.

This complete guide explains why lenders reject applications without collateral, how companies can improve approval chances, and what alternative funding solutions are available for businesses in India.

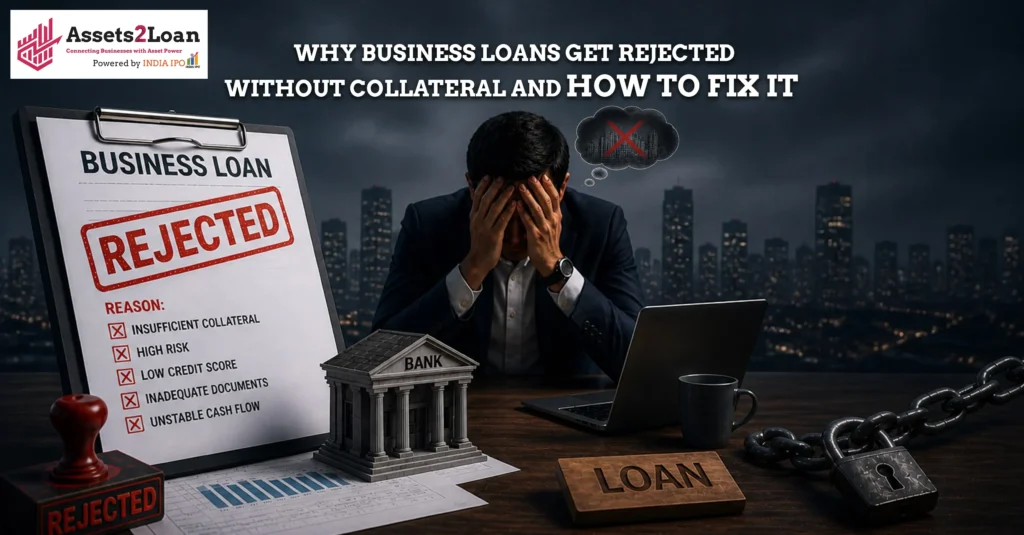

Why Businesses Face Rejection Without Collateral

Most banks consider collateral as a safety mechanism. If a borrower defaults, lenders can recover money by selling the pledged property. Because of this, many financial institutions prioritize secured lending over unsecured exposure.

The most common reasons for Business Loan rejection include:

- Lack of land or property ownership

- Poor credit history

- Weak cash flow records

- High existing liabilities

- Incomplete documentation

- Low business vintage

- Unclear business plans

- Risky industry classification

According to multiple financial lending reports, insufficient collateral remains one of the biggest reasons why MSMEs fail to secure large-ticket funding.

For businesses seeking loans above ₹50 lakh or ₹1 crore, lenders often insist on immovable property security. This creates a major challenge for modern businesses operating on leased infrastructure or asset-light models.

The Growing Problem for Indian MSMEs

India’s MSME sector contributes significantly to employment generation and GDP growth. Yet, a large portion of small and medium enterprises remain underfunded because they lack acceptable collateral.

Industries commonly affected include:

- IT and software companies

- Logistics businesses

- E-commerce brands

- Trading companies

- Service-sector enterprises

- Manufacturing units on leased premises

- Startups and emerging businesses

Many of these businesses are profitable and scalable but do not own land or buildings. Traditional lenders still follow the old mindset:

“No property means high risk.”

This outdated approach creates funding gaps that slow down business expansion and innovation.

What Happens When a Business Loan Gets Rejected

Loan rejection impacts businesses far beyond immediate financing problems.

1. Expansion Plans Get Delayed

Companies may postpone factory expansion, machinery upgrades, hiring, or inventory growth because funding is unavailable.

2. Cash Flow Becomes Unstable

Working capital shortages affect operations, vendor payments, and employee salaries.

3. Growth Opportunities Are Lost

Businesses miss profitable market opportunities while competitors with better collateral move ahead.

4. Higher Borrowing Costs

Many businesses turn to expensive private financing with higher interest rates after bank rejection.

5. Credit Confidence Drops

Repeated loan rejections can negatively affect future lender confidence and create hesitation among investors.

This is why preparing the right funding structure before applying for a Business Loan is extremely important.

Can You Get a Business Loan Without Collateral?

Yes. Businesses can still secure funding without owning property, but approval depends on several factors such as:

- Business turnover

- GST filings

- ITR records

- Banking transactions

- Credit profile

- Cash flow stability

- Existing liabilities

- Industry category

Collateral-free business loans are generally categorized as unsecured loans. These loans are offered based on repayment capability rather than property security.

However, unsecured loans usually have:

- Lower funding limits

- Higher interest rates

- Shorter repayment tenures

- Stricter eligibility checks

For larger funding requirements, lenders may still seek alternative security arrangements.

Alternative Funding Solutions for Businesses Without Collateral

Modern financing models are helping businesses overcome collateral limitations in smarter ways.

1. Third-Party Collateral Funding

One of the fastest-growing financing solutions in India is third-party collateral.

In this structure, a trusted individual or entity provides property security on behalf of the borrower. The property owner remains separate from the borrowing business.

This method is commonly used by:

- MSMEs

- Manufacturing businesses

- Contractors

- Infrastructure companies

- Expanding enterprises

Third-party collateral structures are increasingly helping companies secure high-value Business Loan approvals.

2. Collateral Partnership Platforms

Modern platforms now connect businesses with verified collateral providers.

For example, Assets2Loan helps businesses become “asset-ready” by enabling structured collateral-backed funding solutions.

Instead of forcing companies to buy land, such platforms help businesses:

- Access verified landowners

- Structure secure funding partnerships

- Improve lender confidence

- Raise larger funding amounts

- Preserve ownership control

This model is becoming increasingly popular among growth-stage businesses.

3. Invoice Financing

Businesses with strong receivables can raise working capital against unpaid invoices.

This is especially useful for:

- Suppliers

- Manufacturers

- B2B companies

- Government contractors

Invoice financing reduces dependence on fixed collateral.

4. Equipment Financing

Machinery and equipment themselves can act as security in certain financing models.

Industries commonly using this include:

- Manufacturing

- Construction

- Logistics

- Engineering

Equipment-backed financing helps businesses avoid pledging land assets.

5. Government MSME Loan Schemes

Government-backed MSME schemes often support collateral-free funding under specific eligibility criteria.

Popular schemes include:

- CGTMSE-backed loans

- Mudra loans

- Stand-Up India

- Startup India funding support

These schemes aim to reduce dependency on property-backed lending.

How to Improve Business Loan Approval Chances

Even if your business lacks collateral, proper preparation can significantly improve approval probability.

Maintain Strong Financial Records

Lenders evaluate:

- GST returns

- ITR filings

- Profit & loss statements

- Balance sheets

- Banking transactions

Transparent financial records build lender confidence.

Improve Credit Score

A strong CIBIL score increases approval possibilities for both secured and unsecured loans.

To improve creditworthiness:

- Pay EMIs on time

- Reduce credit utilization

- Avoid multiple loan inquiries

- Clear overdue accounts

Prepare a Detailed Business Plan

A professionally prepared business proposal should include:

- Revenue projections

- Market opportunity

- Business model

- Loan utilization purpose

- Repayment strategy

Weak business plans are among the leading causes of rejection.

Reduce Existing Debt Burden

High existing liabilities negatively impact debt-to-income ratios.

Lenders prefer businesses with manageable repayment obligations and healthy cash flow.

Choose the Right Funding Partner

Different lenders specialize in different funding categories.

Some lenders focus on:

- MSME loans

- Startup funding

- Working capital

- Invoice financing

- Asset-backed lending

- Structured funding

Applying to the wrong lender increases rejection chances unnecessarily.

Common Mistakes Businesses Make While Applying

Businesses often unknowingly weaken their own loan applications.

Applying for Unrealistic Loan Amounts

Overestimating funding requirements raises lender concerns.

Incomplete Documentation

Missing records delay processing and reduce approval confidence.

Frequent Loan Applications

Too many credit inquiries negatively affect credit profiles.

Ignoring Cash Flow Stability

Revenue consistency matters more than temporary profitability spikes.

Hiding Existing Liabilities

Lenders conduct detailed financial verification.

Transparency is critical.

Are Unsecured Business Loans Safe?

Yes, if structured correctly.

However, businesses should carefully evaluate:

- Interest rates

- Processing fees

- Hidden charges

- Repayment flexibility

- Prepayment conditions

- Personal guarantee clauses

Some unsecured lenders may require:

- Personal guarantees

- UCC-style asset rights

- Director guarantees

- Cash flow monitoring

Understanding the loan structure before signing agreements is essential.

Why the Future of Business Lending Is Changing

India’s financial ecosystem is gradually shifting from purely asset-based lending toward cash-flow-based lending.

Modern lenders increasingly evaluate:

- Business performance

- Revenue stability

- Digital transactions

- GST compliance

- Banking patterns

- Market scalability

This transition is creating more opportunities for asset-light businesses to secure funding.

Technology-driven underwriting and structured collateral partnerships are expected to dominate future Business Loan approvals in India.

Final Thoughts

A rejected Business Loan application does not mean your business lacks potential. In many cases, businesses are rejected simply because they do not own the type of assets traditional lenders prefer.

Today, multiple financing alternatives are available for businesses without collateral, including:

- Third-party collateral

- Structured funding partnerships

- Invoice financing

- Equipment funding

- MSME government schemes

- Collateral partnership platforms

The key is understanding how lenders evaluate risk and preparing your funding structure strategically.

Businesses that maintain strong financial discipline, transparent documentation, and smart funding planning can still secure large-scale capital successfully — even without owning land or commercial property.